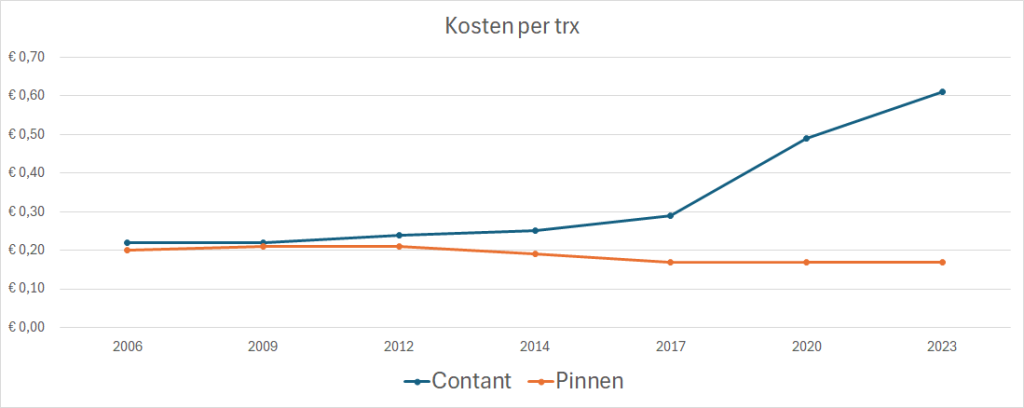

Rising cost differential between debit card and cash at the counter

The differences in payment costs at the counter for entrepreneurs, between cash payments and debit card payments, increased sharply between 2017 and 2023. In 2017, a typical entrepreneur paid €0.29 per cash payment and €0.17 per debit card payment. By 2023, the cost of a cash payment had more than doubled to €0.61 while that of a debit card payment remained the same at €0.17. A cash payment now costs an average entrepreneur more than three times as much as a debit card payment. This emerges from periodic surveys by Panteia, commissioned by Betaalvereniging Nederland and Dutch point-of-sale establishments (retail trade, hotels and restaurants, petrol stations and street trading).

The differences in costs for cash payments between branches of point-of-sale establishments also increased further in the same period. In 2017, a hospitality entrepreneur paid roughly twice as much for a cash payment (€0.47) as a retailer (€0.24). By 2023, that difference has increased to almost three times as much (€1.36 in the hospitality sector and €0.50 in the retail sector). This is partly due to relatively efficient cash handling in the retail sector.

The increase in smooth contactless payments, usually without a PIN, at the expense of the slower insertion with a PIN, has kept the cost of a typical PIN payment at a consistently low level for years. As a result, PIN payments at the till remain the most efficient form of payment for society.

Payment costs consist mainly of labour costs

More than half of the total cost of a typical payment at the counter consists of internal costs (60%, €0.17), including in particular employee labour costs. The work that payments entail includes settling at the cash register, making up the cash register daily and transporting and depositing cash themselves. Especially for point-of-sale establishments in SMEs, internal costs weigh heavily. With cash payments, these internal costs amount to 79% of the total costs (€0.48 per payment). With contactless debit card payments, it is only 55% (€0.09 per payment).

The costs of external services for point-of-sale entrepreneurs (by banks, payment institutions, telecom companies and money transporters) amount to an average of €0.13 for a cash payment and €0.08 for a contactless debit card payment.

Cost of average point-of-sale payment

The number of relatively cheap debit card payments at the POS increased sharply between 2017 and 2023 ( 47%), at the expense of expensive cash payments (-52%). As a result, the average payment cost for entrepreneurs rose by only 22%, from €0.23 to €0.28 per point-of-sale payment. The average amount per payment rose by 32%, from €19.85 to €26.22. Inflation was over 26% in the same period, which entrepreneurs see reflected in, for example, higher wage costs and purchase prices.

Cash payments can be more efficient

Since 2017, the annual number of cash payments in the four retail sectors surveyed has more than halved. The total payment costs for cash have increased slightly during that period. In particular, total internal costs (roughly €560 million per year) for cash-related operations have not decreased (for making up cash registers and carrying and depositing cash sales themselves). Despite the declining use of cash, entrepreneurs are not scaling down the associated work to the same extent.

Therein lies room for greater efficiency, for example by deploying smart cash machines at the counter, combined with professional cash transportation (including depositing cash turnover and withdrawing change). Large retail outlets and petrol stations with high turnover make more use of this than small catering businesses and market traders with relatively small turnover. Partly because of this, the former branches have realised significantly lower relative payment costs for cash payments (2% of cash turnover) than the other two branches (6% of cash turnover) since 2017.

Related articles

-

Stakeholder Forum looks (far) ahead

-

News

-

European legislation

-

-

DNB presents ‘Payments Strategy’ until 2028

-

News

-

Availability and disruptions

-

-

Arjan Bol on Radio 5 about deferred card payments

-

News

-

Availability and disruptions

-

-

Consumers increasingly buy online via smartphone

-

News

-

Online payments

-

-

Scams tap into migration of iDEAL to Wero

-

News

-

Online payments

-

-

Payments newsletter: Betaaljournaal 34

-

Payments newsletter

-