Payment cards

Almost everyone has a debit card linked to a checking account. With a debit card, we can pay easily and safely in shops, restaurants and petrol stations, among others, and withdraw cash from ATMs.

When using a debit card, the amount is debited directly from the cardholder’s payment account. This differs from credit cards, where payments are settled with the cardholder later, usually at the end of each month.

From magnetic strip to payment chip

The first generation of payment cards featured a magnetic strip. The cardholder pulled the card through the card reader of the payment terminal and entered his PIN. However, the magnetic strip proved easy to copy (skim), causing a lot of damage from skim fraud between 2005 and 2012.

Partly to reduce this skimming fraud, all payment cards were given an EMV payment chip and, since 2012, we have only paid with this payment chip in Europe. All card data are safely encrypted on that chip and cannot be read or copied by unauthorised persons.

From insertion to contactless

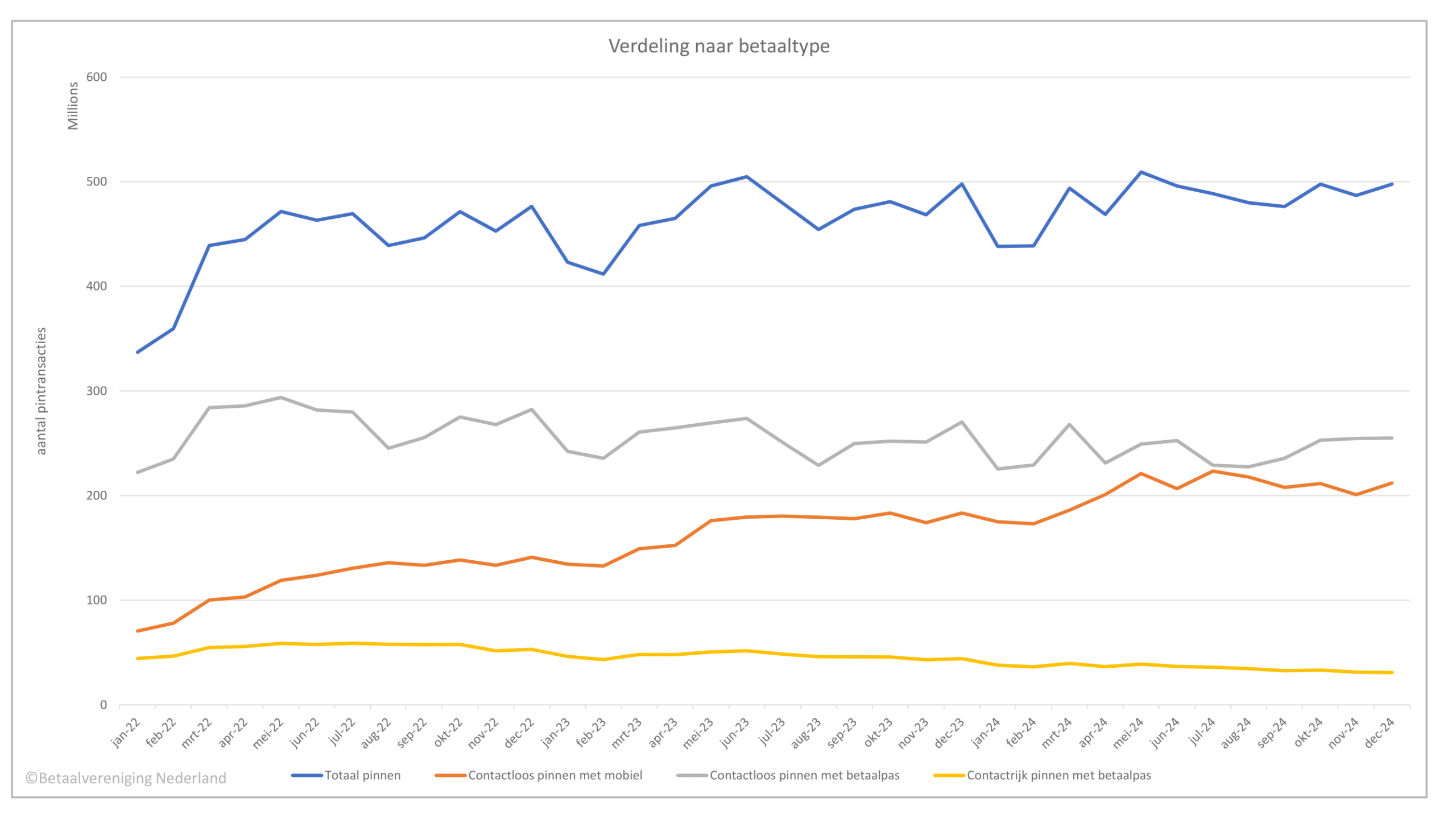

To make paying even easier, contactless payment cards were introduced in 2013. The card no longer needs to be inserted into the payment terminal and only briefly held against the card reader. For amounts up to €50, no PIN code is usually needed.

From 2015, contactless payments were also possible with a digital debit card on a smartphone or smartwatch. Paying is done by holding the device briefly to the payment terminal, after unlocking it with a numerical code, fingerprint or facial recognition.

Renewed payment cards

Many payment cards still carry the card brands V PAY and Maestro. However, banks are gradually switching to the Debit Mastercard and Visa Debit card brands. Those card brands are accepted in more places outside Europe and you can also use them to pay online.

For cardholders, little will change. Within Europe, you can pay and withdraw money with a renewed debit card in the same way as with an old debit card. Everyone will receive an updated debit card automatically, you do not need to do anything yourself.

Features of the renewed debit card

- In addition to the IBAN, there will be a card number of 16 digits or more on the card (a PAN) and a security number of 3 or 4 digits.

- There is “Debit” on the card to clearly indicate that it is not a credit card.

- A tactile notch helps visually impaired people recognise the card and enter it correctly.

This content is available after accepting the marketing cookies.

Life cycle of debit cards

Payment cards are purchased by banks from card suppliers. They are now routinely made of recycled PVC; experiments are also under way with biodegradable materials.

Each card has an EMV chip with an NFC antenna for contactless payment (Near Field Communication). A new debit card is valid for up to five years but can also be replaced earlier due to malfunction, loss or theft. When the expiry date approaches, the cardholder’s bank will automatically send a replacement debit card. The cardholder does not have to do anything for this himself.

After using a new payment card, the cardholder can cut the old card – right through the payment chip – and throw it away as plastic waste. Old payment cards are not recycled.

Future prospects

More and more cardholders are paying with a digital payment card on their smartphone or smartwatch. By 2025, half of all Dutch contactless payments were with a mobile phone or smart wristwatch, and this is increasing further.

European banks are working on a new European payment method called Wero. The future should show how this will affect the use of current debit cards, at the counter and online.