Many cash laws and regulations forthcoming

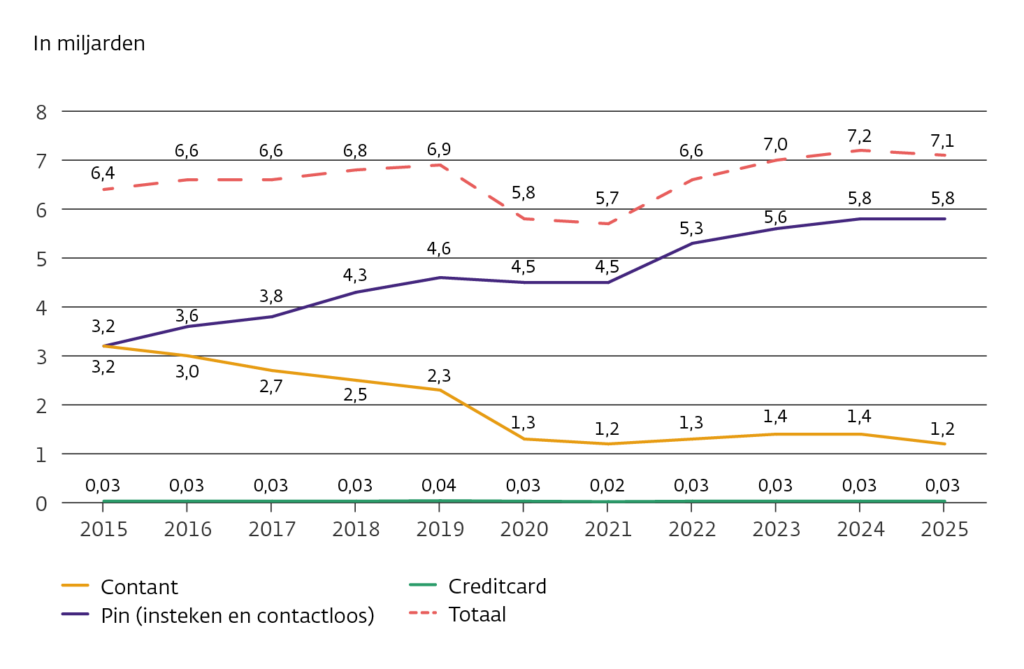

Cash was still the most commonly used means of payment at the counter in the Netherlands until 2015 (54% of all payments in 2014). Ten years later – in 2024 – only one in five transactions at the checkout will be paid for in cash. The remaining four transactions will be made electronically, with a (contactless) payment card or with a mobile phone.

The accessibility, availability and safety of cash is fodder for social and political debate. That discussion is also held within the MOB ( Maatschappelijk Overleg Betalingsverkeer chaired by DNB, the Dutch Central Bank). In recent years, the MOB has been calling for cash to remain easily accessible and usable for everyone who needs it.

Political measures, in the Netherlands and in Europe

The public debate and a study by DNB have also prompted politicians to define legal frameworks for a society with ‘less cash‘ without becoming completely‘cashless‘. This discussion is not only ongoing in the Netherlands; there are similar challenges, discussions and measures within the EU.

Directives, agreements and legislation

Since roughly 2020, a lot has happened around cash and we see various developments and measures coming our way. We would like to provide an overview of these.

1. Geldmaat

Since 2011 Geldmaat (formerly GSN or Geldservice Nederland) handles cash money traffic on behalf of ABN AMRO, ING and Rabobank. Geldmaat manages and maintains almost 4,000 ATMs and deposit safes throughout the country.

At some ATMs you can only withdraw banknotes. Other ATMs can also deposit banknotes or withdraw and deposit coins. Cardholders of almost all banks worldwide can withdraw euro notes at Geldmaat’s ATMs.

Business owners who are customers of ABN AMRO, ING or Rabobank can deposit large amounts of cash in so-called ‘sealbags’ at special Geldmaat deposit vaults.

Cardholders of ABN AMRO, ING, Rabobank, SNS and ASN Bank can deposit notes at many Geldmaat ATMs. Cardholders of only ABN AMRO, ING and Rabobank can also deposit and withdraw coins at Geldmaat, at suitable ATMs.

2. Five-kilometre standard

The five-kilometre ATM standard states that most Dutch people should be able to withdraw cash from an ATM within a radius of five kilometres from their home address. This norm has existed since 2006 based on a MOB agreement and came about as a result of the Crone bill for basic payment services . To date, this standard is used and adhered to by Geldmaat.

Between the three major banks (the owners of Geldmaat) and DNB, it was agreed that no more than 0.3 per cent of all Dutch citizens should fall outside this norm. In particular, remote homes in sparsely populated areas sometimes fall outside the norm.

3. Cash Covenant

In 2022, the Cash Covenant was concluded under the direction of DNB. These agreements aim to ensure that cash continues to function well as a means of payment at the physical cash register. The covenant was signed by the major banks, by Betaalvereniging Nederland, by representatives of consumers, retailers, hotels, restaurants and petrol stations, by cash transporters and processors and by DNB. The agreements in the covenant apply for a period of five years, until 2027.

The covenant includes many provisions for banks and Geldmaat to keep cash readily available, accessible and affordable for consumers and entrepreneurs.

The covenant requires specific counter establishments to always accept cash from customers. This applies in particular to municipal counters, pharmacies and other establishments for which consumers cannot easily find an alternative nearby.

4. Dutch Cash Bill

In the Cash Covenant, it was also agreed that DNB and the Ministry of Finance will commission a study on how to safeguard the public interest in cash after the covenant expires. In May 2023, the results of this study were published in the report‘Future design of the cash chain‘ (TICKET).

The research report states that the long-term cash infrastructure cannot be offered at a socially desirable level on the basis of voluntary agreements, such as a covenant. Presenting the TICKET study to the House of Representatives, the finance minister adopted that conclusion: legislation is needed so that cash remains readily available, accessible, affordable and usable as a means of payment for consumers and entrepreneurs. To this end, the minister is now working on a bill requiring banks to maintain that infrastructure accessible and affordable for end users. The bill should also ensure that money transport remains reliable and readily available.

More concretely, the Money Bill includes the following measures:

- Major banks must maintain a nationwide basic infrastructure of ATMs.

- Many banks will be obliged to offer their current account holders access to this basic infrastructure, at maximum rates for business owners and free of charge for consumers. Only small banks with fewer than 50,000 account holders in the Netherlands will be exempt from this.

- CIT in the Netherlands is currently largely carried out by one service provider. To ensure the continuity of CIT, DNB will monitor it. Large cash transporters must report periodically to DNB on their financial health.

- DNB must monitor and enforce the obligations in the bill.

The Dutch Chartaal bill does not include rules on the acceptance of cash by point-of-sale establishments because there is an EU bill for that. The Netherlands is in favour of an acceptance obligation, provided it is proportionate and feasible for point-of-sale establishments .

After a public consultation, the Dutch bill was slightly modified and sent to the Council of Ministers in June 2024. After agreement by the Council of Ministers, the Council of State issued an opinion on 21 October 2024, limited to some suggestions and general advice.

The opinion of the Council of State is not binding. The minister does have to let it be known in a ‘further report’ whether and how it intends to incorporate the advice into the bill. The bill then goes to the House of Representatives, together with:

- an Explanatory Memorandum;

- the advice of the Council of State;

- the minister’s ‘further report’;

- a Royal Message.

With the Royal Message, the king presents the Chartal Public Bill to the House of Representatives. In the House of Representatives, the bill is first debated in writing by a specialised committee. The minister then defends the bill in a plenary debate. The debate is followed by a first vote on any proposed amendments, followed by a vote on the entire bill. If the bill is passed, it goes to the Senate.

Content

The content of the final Charter Act is not expected to be much different from the original bill. Of this, it was already known that several details will be worked out in AMvBs (Orders in Council). It is not yet clear for which details this will apply. It is possible that accessibility standards and pricing rules will be included in AMvBs, based on the agreements in the Cash Covenant.

Timeline

The Cash Bill is expected to be tabled in the Lower House in the first quarter of 2025 after which it will be debated in the Lower and Upper Houses of Parliament. The bill could then be passed in January 2026 at the earliest and otherwise in July 2026.

5. Money laundering prevention plan law and ban on cash payments for goods above €3,000

The Amendment to the Prevention of Money Laundering and Financing of Terrorism Act (Wwft) proposes a ban on cash payments for goods above €3,000. For this, the Ministry of Finance made a proposal to amend the ‘Money Laundering Action Plan’ to maintain only a ban on cash payments from €3,000 or more. The aim of this ban is to make money laundering more difficult.

Cash payments are a common way for criminals to launder money. That is why there will be an EU-wide ban on cash payments above €10,000 for transactions with and between traders and service providers by 2027.

Many EU countries already have limits on cash payments that vary between member states. Countries with a lower limit than €10,000 are given room to keep it. The Netherlands wants a ban on cash payments above €3,000 for transactions with and between traders.

Traders in goods are already required to carry out customer due diligence on cash payments above €10,000. They must report unusual cash transactions above €10,000 to the FIU. This obligation will disappear for many merchants with the introduction of the ban. This will reduce the administrative burden on these traders.

Content:

- The ban only applies to transactions with or between traders in goods, such as shopkeepers.

- Private individuals who sell something to another private individual, for example through Marketplace, are not covered by this ban.

- The ban applies to all traders buying or selling goods. There are no exceptions for specific sectors.

- The ban does not apply to offering services. There will be European regulations in 2027 that will still ban cash payments for services.

- The limit of €3,000 was chosen based on what has been established in the countries around us. With this, the government wants to prevent criminals from trying to launder money in neighbouring countries or precisely in the Netherlands.

- This €3,000 limit makes it more difficult for criminals to launder large sums of money. At the same time, it provides room for citizens to settle many purchases in cash.

- Bureau Toezicht Wwft will monitor compliance with the ban. After 3 years, there will be an evaluation into the functioning of the ban. The bureau will also investigate circumvention of the ban.

Timeline:

The bill ‘Money Laundering Plan’ was tabled in October 2022 and passed through various intermediate stages by the House of Representatives in September 2024. On 10 June 2025, the bill was passed by the Senate.

The aim is to implement the ban by 1 January 2026. The amendment and the effective date are part of the Netherlands’ fulfilment of the ‘Recovery and Resilience Plan’. If the Netherlands fails to meet the milestones in the‘Recovery and ResiliencePlan ‘, it will miss out on an EU sum of up to €600 million.

6. Amendment compulsory underwriting

In the parliamentary debate on the ‘Money Laundering Plan’ bill on 24 September 2024, MPs van Dijk and Flach tabled an amendment for a cash underwriting obligation of up to €3,000. That the amendment was tabled for the Money Laundering Plan Bill and not for the Cash Bill is rather surprising. The amendment was passed by 81 votes out of 150 .

Content

- The amendment is part of the amended money laundering plan bill.

- In principle, the underwriting obligation applies to any publicly accessible location or institution that offers paid products or services to individuals.

- The government is given the option of using AMvBs to establish exceptions to this acceptance obligation on a sector-by-sector basis, if it is adequately substantiated that this is necessary for performance or safety.

Timeline

- The Senate submitted written questions to the finance ministry.

- The minister in turn asked the ECB (European Central Bank) for an opinion on the Dutch amendment and has since received this opinion. For the time being, the ECB sees scope for a national underwriting requirement.

- The process includes ‘pre-hearing’* in the Lower and Upper Houses and an internet consultation.

- The amendment will not be voted on separately when considered in the Senate. The Upper House will say ‘yes’ or ‘no’ to the entire Lower House proposal – including the amendment.

- The acceptance obligation will come into force only after the exception decision(s) are adopted.

- The drafting of this decision is expected to take more than a year, until 2026.

* ‘Preview’ means that First or Lower House members can ask for 30 days to submit an AMvB as yet in the form of a bill.

7. European cash bill

Cash is also an important issue in the European Commission. In June 2023, just before the summer holidays, the European Commission submitted a legislative proposal (regulation ) called the Single Currency Package . Part of this legislative package is a regulation on the legal tender properties of euro banknotes and coins. That in turn is part of the digital euro package, which aims to supplement physical central bank money with a digital variant.

The proposal would give the digital euro legal tender status, including an acceptance obligation, with acceptance of the physical euro also guaranteed for the first time in secondary legislation. However, exceptions to the acceptance obligation are possible.

At present, it is difficult to establish a reliable timeline for the bill. Council meetings required for this were scheduled for 2024 but have still not taken place by early 2025.

Content

“Euro banknotes and euro coins presented for payment of a monetary debt by the debtor must be accepted.”

- Acceptance mandatory for full face value.

- Charging of additional fees not allowed.

- Not applicable to online purchases.

- Exceptions:

- If a refusal is made in good faith and is based on a good and timely announced reason. For example, if value of a banknote offered disproportionately exceeds the amount of the debtor and in case the creditor has no change available.

- Article 7 (‘Acceptance of payments in cash’) of the bill leaves room for unilateral exclusion (for the individual counter operator) but obliges Member States to monitor and take measures (at national, regional or sectoral level).

- The ECB opinion on the proposal argues for no unilateral exclusion at all (paragraphs 2 and 3). This leaves the question of what the final legislation will look like; it could still go either way on the issue of unilateral exclusion.

- Once the regulation enters into force, all euro area member states will have to monitor the access to and acceptance of cash on their own territory. They must also report annually on their supervision to the European Commission and the ECB, and take corrective measures if necessary.

Timeline

- Negotiations are ongoing but slower than expected. No precise timeline can be given for this.

- The regulation is subject to the ordinary legislative procedure, which means that both the European Parliament and the European Council must consider and adopt the regulation before it can enter into force.

In general, a European law (regulation) takes precedence over a member state’s law. This would mean that only the European acceptance obligation would apply. How the Dutch and the European acceptance obligation relate to each other is difficult to assess for the time being. For the time being, the Dutch amendment seems to pre-empt the European acceptance obligation, which may not come into force until 2027 or even 2028.

All legislative proposals at a glance

Timeline of developments for cash

- 2006: Introduction of five-kilometre standard for cash dispensing points

- 2015: More debit card payments than cash payments at Dutch counters for the first time

- Since 2019: ATMs of ABN AMRO, ING and Rabobank slowly give way to ATMs of Geldmaat

- April 2022: Signing of Cash Covenant

- October 2022: Legislative proposal ‘Plan to tackle money laundering’ and ban on cash payments for goods above €3,000

- June 2023: European legislative proposal on cash as legal tender

- 2023: Results TICKET survey lead to legislative proposal on cash

- June 2023: Additional agreements Cash Covenant

- September 2024: Amendment to legislative proposal ‘Plan to tackle money laundering’, for obligation to accept cash up to €3,000

- October 2024: Council of State opinion on Chartaal bill;

- opinion contains no significant objections

- November 2024: Amendment compulsory acceptance adopted

- Q1 2025: ‘Money laundering action plan’ debated in Senate

- Q1 2025: Chartaal bill tabled in Lower House and debated in Lower and Upper Houses of Parliament

- Q1/Q2 2025: Consultation on legislative proposal ‘action plan to combat money laundering

- Q3 2025: Consideration of European bill on cash as legal tender

- Q3/Q4 2025: Consultation AMvBs accompanying the Money Laundering Act

- Q1 2026: envisaged effective date of Chartaal Act

- Q1 2026: Intended effective date of ban on cash payments for goods, to professional traders, from €3,000 onwards

Related articles

-

Elderly increasingly pay with debit card

-

News

-

Card payments

-

-

Trial with €100 banknotes at Geldmaat

-

News

-

Cash payments

-

-

DNB payment figures available for 2025

-

News

-

Account-to-Account payments

-

-

DNB presents ‘Payments Strategy’ until 2028

-

News

-

Availability and disruptions

-

-

Make sure you have (digital) fallback options in case of a potential card payments failure!

-

News

-

Card payments

-

-

Arjan Bol on Radio 5 about deferred card payments

-

News

-

Availability and disruptions

-